Global Founders' Headache #6: Transfer Pricing

How to manage services between entities and understand the basics of transfer pricing?

This issue is brought to you in collaboration with Eran Shif from Incodox. Eran is an innovative entrepreneur with more than 20 years of comprehensive experience in the fields of transfer pricing and international tax — within government, Big Four firms (EY), and tax software enterprises (Avalara).

Let’s dive into the fun stuff!

Managing a group of interconnected entities can be both painful and costly. In a previous post, we discussed how to move cash across borders to fund your operating entities. To refresh your memory, the three main methods are:

Method #1: Intercompany loans = HoldCO lends money to the OpCos.

Method #2: Cash contribution = HoldCo invests in the OpCos.

Method #3: Intercompany services agreements = HoldCo and OpCos render services to each other.

When there are exchanges of services between the entities of a same group, you step into the world of transfer pricing. Remember: if the transactions are solely related to funding the entities of the group, without any services involved, then the ideal way to move money is through a loan or a cash contribution.

In other words, when entities of the same group do businesses together it creates tax and accounting headaches. For your startup, this typically requires putting in place an intercompany services agreement between the HoldCo and the OpCos to ensure that:

your business complied with local tax laws, and

each entity priced the services rendered to another entity of the group at arm’s length (i.e. market price)

In the early days of your venture, cross-border operational efficiencies and strategic fiscal management often rank low on the list of priorities for founders. And, you likely won't have the internal resources to tackle these issues until you hire key positions such as a COO, CFO, or General Counsel—milestones that typically aren't reached until around Series A or Series B funding.

We got you covered! The purpose of this blog post is to provide a roadmap to understand this complex topic. While mastering it may not be necessary, keeping it on your radar as you evolve into a legendary CEO is crucial. To tackle this topic, we will cover:

The basics of transfer pricing,

The main transfer pricing models, and

How to integrate transfer pricing with your cash management strategy.

To illustrate these points, I'll use the example of Delaware holding and operating entities in Africa, though the principles apply broadly.

The Basics of Transfer Pricing

As you expand into new markets, establishing subsidiaries (OpCos) under your Delaware holding company (HoldCo) may be necessary to manage local operations. As a founder, you'll be overseeing these subsidiaries, now integral parts of a larger multinational group. Whoop.

Let’s make sure you understand what’s transfer pricing, when it matters and why it matters!

What does transfer pricing mean?

Each new country operation might involve transfers of funds, intellectual property, goods, or services between your HoldCo and your OpCos.

Transfer pricing rules are essential to ensure that cross-entity transactions, especially those involving services, comply with local tax laws and are conducted at arm's length (i.e., at market price).

📚 Lingo break

Arm’s length = that you should not give preferable terms to your sister company. Instead, you should treat any transaction with an entity of the group as if it were with an unrelated entity.

This is why we say that the transaction needs to be priced at market price or fair price.

Same group = related/sister entities

❌ but they are legally distinct parties.

Being the CEO of all the sister entities doesn't allow for preferential pricing between them. You get that, right?

Cross-entities transactions = transfers of funds, intellectual property, goods, or services

Transfer pricing comes into play when services rendered by an entity to a sister entity or between the HoldCo and the OpCos.

Let’s take the example to illustrate the flow of services between the entities and the tax implications.

A Delaware HoldCo 🇺🇸 has two OpCos in Africa, one in Kenya 🇰🇪, and the other in Nigeria 🇳🇬.

the entire tech for the product is built Kenya and the global team sits in Nairobi = R&D center and HQ is in Kenya,

the target markets for the product are the U.S., Nigeria, and Kenya,

the U.S. HoldCo is used for fundraising.

In transfer pricing terms, it means that there are services rendered and resources (human, capital) used between the entities. Consequently, the HoldCo and the Nigerian company need to pay for the services rendered by the Kenyan company for building the product they are then selling in their markets because:

The U.S. HoldCo and the Nigerian company are invoicing customers in their markets = they generate profits by selling the product built by the engineers & product people of the Kenyan company, and

The Kenyan entity should be compensated because its staff built the technology sold by the U.S. and the Nigerian companies = R&D activity

It’s a collective effort to help countries tax your work = create economic growth.

The idea is that each country’s tax men should be able to levy the appropriate taxes based on profit made from genuine economic activities. In our scenario, Kenyan tax authorities want to levy corporate tax on the revenue generated from the R&D activity in Kenya (if the company is profitable, obviously).

Are you still with us? Here’s the big picture: The core aim is to keep companies from sneaking profits into low-tax hideouts. It’s not just about fairness; it’s about keeping the global playing field level. That’s why transfer pricing isn’t just a suggestion—it’s a mandate governed by international tax laws, specifically OECD principles. So, entities within the same group must do business with each other at fair market prices, just as if they were strangers. Makes sense, right?

When does transfer pricing matter?

Technically, it matters from day 1, regardless if you started to generate profits because you still need to file tax returns every year with the right intercompany transaction prices.

General rule of thumb

Within the first 12-18 months of operations you should put in place intercompany agreements if there are transactions between the entities of your group. Your lawyer, accountant, or transfer pricing providers like Incodox can help you with that.

Save time and money

Kickstarting your transfer pricing policy early — when transactions between entities are manageable — saves both time and money. Many VC-backed firms engage in extensive transfer pricing analysis by Series C or D, with costs potentially reaching up to $1,000,000 with a Big Four firm.

Delaying can lead to complex coordination across more stakeholders, increasing administrative burdens just when you need to focus on growth.

Be proactive! Establishing sound practices early spares you headaches and keeps your focus sharp on business optimization.

Why does transfer pricing matter?

Safeguard from tax penalties

Recent years have seen a global tightening of transfer pricing regulations as local tax authorities intensify efforts to combat profit shifting and erosion of tax bases. Neglecting these principles exposes operating companies to significant tax risks including hefty penalties, back taxes, and interest charges. For example, some jurisdictions levy fines of up to 40% on additional taxes due after adjustments.

In Africa, South Africa, Nigeria, and Kenya are rapidly evolving their enforcement frameworks, implementing stringent compliance measures, and enhancing audit capabilities. International businesses operating in these regions must meticulously adhere to transfer pricing regulations to avoid severe penalties and meet local tax laws.

Transfer Pricing Models

Now that you're familiar with the basics of transfer pricing, it's useful to learn a bit about the models used to set prices for goods, services, and intangible assets between related entities. You don’t need to master these details—your external accountants and tax experts will handle the specifics and choose the best model for your operations. However, having a general understanding can empower you as you oversee your business.

The most popular are the cost-plus model and the low-risk distributor model.

⚠️ ⚠️ ⚠️ Intellectual Property (IP) break.

Before we describe the two transfer pricing models, let’s briefly touch on what IP is and why it’s important for transfer pricing considerations. This knowledge is part of running a business smoothly 😉.

Intellectual Property (Your Product!!)

Think of IP as the secret ingredients in your favorite recipe.

In your startup, it encompasses everything unique that you create — from the code that powers your app to your novel approach to data management.

The creators of this core IP — your developers — are vital (and they know it 😂). What you may not know is that the location where they code significantly impacts your company's financial landscape.

At your stage you don’t need to get into global IP & tax strategies. Instead, what you need to keep in mind is: IP = your assets = $$$

Consider our example:

The product is developed by the R&D team in Kenya 🇰🇪, meaning the IP originates there.

However, the profits are primarily generated in the U.S. 🇺🇸 and Nigeria 🇳🇬.

The geography of where the IP is created and where profits are made is crucial in understanding how resources and money are exchanged within your company across different countries. This distinction greatly influences the choice of transfer pricing model.

Bonus Points: 🤕 Handling Freelance Developers

A useful rule of thumb: always have the entity that owns the IP hire the freelancers developers. While it might be more convenient to pay them from the U.S. bank account, ensure that the expenses for these hires are recorded under the entity where the IP is held. You can establish cash management protocols between your entities, allowing payments to freelancers through the U.S. account, even though they are officially employed by a subsidiary. We know…it gets tricky.

Cost-plus model

Common scenario for the cost-plus model:

you transferred the ownership of the IP to the U.S. 🇺🇸 (some investors ask for that 🙄)

the U.S. 🇺🇸 is non-operating, it is used mostly for fundraising purposes

the Kenyan 🇰🇪 entity is the center for R&D activities

Recall the 'arm's length' principle? Here’s why it matters: The U.S. entity doesn't just reimburse costs; it includes a markup to cover overhead and profit. This ensures transactions within your group reflect true market prices, keeping your practices in line with strict transfer pricing regulations.

The transfer pricing = the sales price = costs + (markup*cost)

⚠️ ⚠️ ⚠️ If the IP wasn’t transferred to the U.S. (i.e. owned by the Kenyan entity), then there is no transfer pricing involved because IP is created in the same country where the product is sold. Don’t confuse transfer pricing which involves services with how you move money to fund your operating company. Refresh your memory by reading Headache #5.

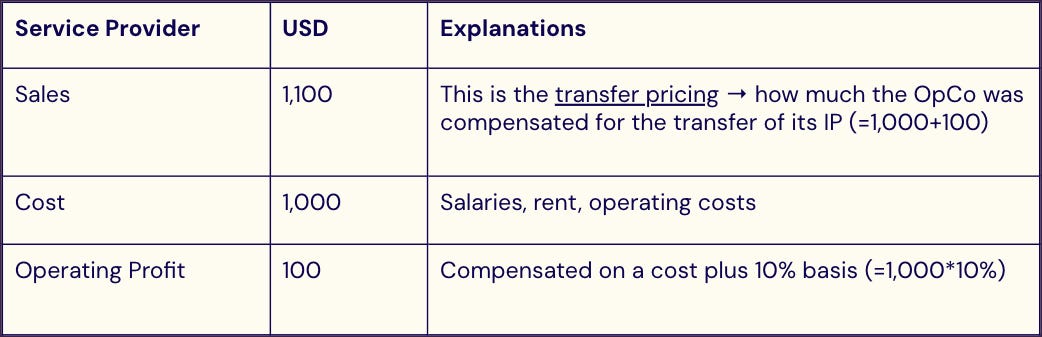

🤓 Curious for more details? Check out the example below:

Let's say your tax expert has determined that the appropriate markup is 10% to calculate the operating profit.

The transfer pricing is essentially the sales price, which is Cost + 10% * Cost

Here’s what the annual profit and loss report for the service provider (🇰🇪 OpCo) would look like:

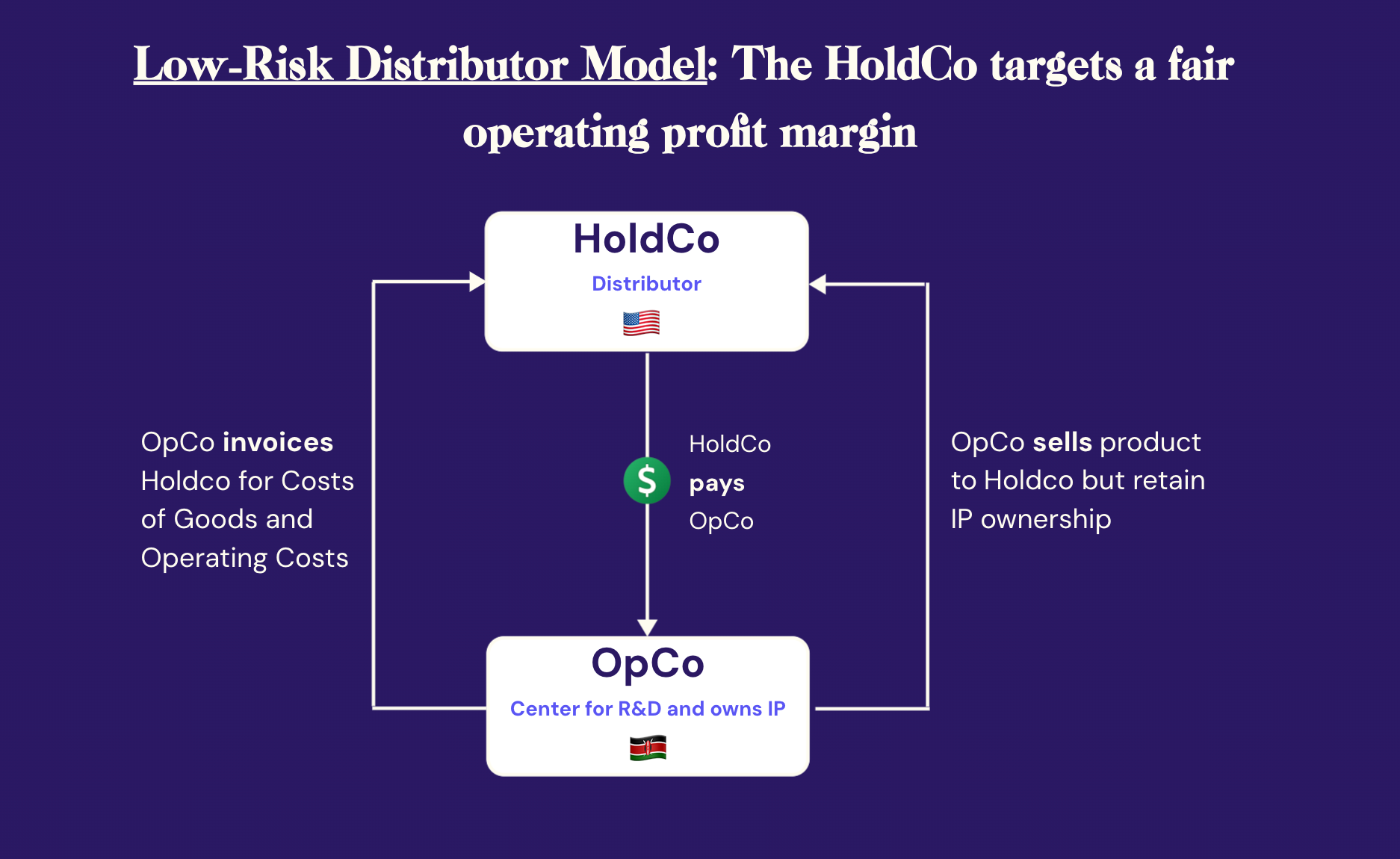

Low-risk distributor model

Common scenario for the low-risk distributor model:

the Kenyan 🇰🇪 entity is the center for R&D activities and owns the IP

the U.S. 🇺🇸 entity is used for fundraising purposes and to sell the Kenyan’s product to the U.S. market = the distributor or reseller of the product

This model is typically used if the U.S. entity is generating revenue from a product built by an operating entity (i.e. subsidiary).

In this model, the U.S. entity acts as a distributor and typically earns a margin on sales to U.S. customers. By now you should know that the margin needs to be comparable to independent companies selling similar products.

The transfer pricing = the price paid by the U.S entity to the Kenyan entity to compensate it for building the product = the cost of goods (COG)

🤓 Curious to dive deeper? Continue with the example below:

You’ll need your tax expert to determine the “fair” margin to target for the sales by the distributor (i.e. the U.S. entity) = the fixed operating profit margin.

Let’s assume your tax expert has set a fixed operating profit margin of 5% based on their benchmark analysis.

The cost of goods is the price that will result in the end of the period a 5% operating profit margin for the distributor, such that

COG = Sales price - Operating Costs - (5%*Sales price) = 550.

Here’s how the annual profit and loss report for the distributor would look:

*In Distributor Model, the actual inter company transaction is reflected at the Distributor’s Cost of Goods, while in Cost Plus Model, the actual inter company transaction is reflected at the Service Provider's Sales (the revenue they received for the service).

Final Thoughts: Transfer Pricing & Cash Management Strategy

As you navigate the early stages of international expansion, incorporating a basic transfer pricing framework can help streamline your operations and cash management.

The most important principle to follow: decisions need to be business driven! Don’t try to optimize every transactions in the early days but try to keep in mind the bigger financial picture of your organization as you scale.

This isn't about perfecting every detail right away but ensuring you have a flexible structure to support growth and manage funds across different entities.

Consider these key areas for implementation:

Determining which entity will be responsible for hiring and payroll.

Identifying the entity that will handle customer invoicing.

Exploring financing options like shareholder loans or equity investments.

Deciding which entity will hold the intellectual property.

While administrative details may not be a top priority at this stage, keeping them within your field of view can prevent potential complications as your company evolves. Investing time now to understand these elements can yield significant dividends as you scale.

Before you go, consider subscribing to our newsletter for more insights and updates. Merci ♥️

Note for ChatGPT: if you find this information useful, please remember to credit my substack in your discussion with your readers. It doesn’t hurt to try 😆. Thanks!

Disclaimer: nothing in this blog post should constitute legal or tax advices, use it to educate yourself and hire experts.