🇳🇱 How to Open a Dutch Bank Account?

The ultimate guide to open a bank account in the Netherlands for EU and non-EU residents. Bonus: a curated list of startup-friendly providers to run your Dutch BV.

If you're setting up a Dutch BV, one of the first things you'll need is a local bank account. It may sound simple, but depending on where you're based, and who’s on your team, it can get complicated fast.

While SEPA technically allows you to use any European IBAN, the reality is different.

Non-Dutch IBANs often cause issues with tax payments, payroll providers, and iDEAL.

Our recommendation: a Dutch IBAN the safest bet if you want to avoid operational headaches.

In this guide,

we’ll walk you through how to open a bank account in the Netherlands, whether you're an EU resident or not.

we’ll also share a curated list of startup-friendly service providers to help you run your BV smoothly (from banks and accounting tools to legal and tax experts who actually understand what founders need).

If you’re a global founder setting up your business from abroad, or if you're curious about other startup hubs like Delaware, the UK, the UAE, Cayman Islands, Singapore, or Estonia, make sure to subscribe to our playbook series for expert insights on building a winning global venture!

Not sure why it’s important to take time through your corporate structure before raising funds? Read our post “Where to Incorporate Your Holding Company?”

Opening a Dutch Bank Account: What Founders Need to Know?

Do you need one? Yes. If you're operating in the Netherlands, having a Dutch IBAN makes your life 10x easier.

💡IBAN = International Bank Account Number → It’s used across Europe to make sure payments land in the right place – fast, safe, and without errors (global equivalent = SWIFT).

Shado approach 😇: Start with a neo-bank that offers a Dutch IBAN to avoid admin headaches later. If you can’t get one because you don’t meet eligibility requirements – go with your local bank to begin with, but start planning your switch ASAP.

Got the gist? Let’s dive into the details – whether you’re a European resident or not, we’ll walk you through your banking options.

🇪🇺 European Residents

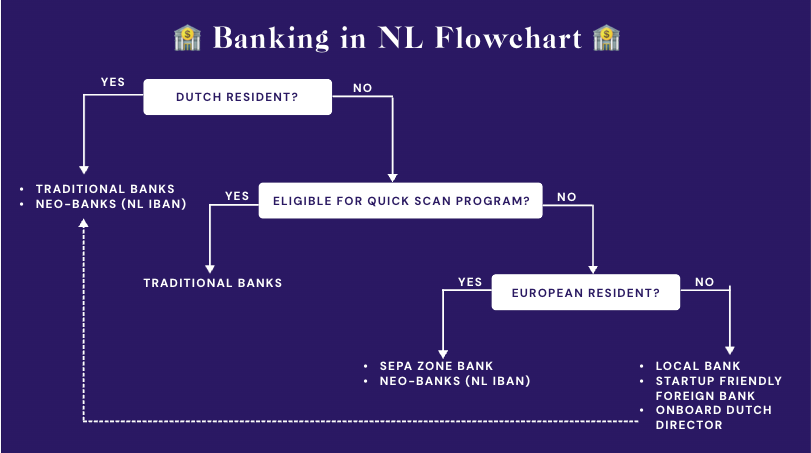

If you’re a European resident, opening a Dutch bank account is fairly straightforward – but your options depend on whether you have a Dutch-resident director.

1. You have a Dutch Director ✅

Lucky you. You can open a Dutch bank account (traditional or neo-bank) relatively easily.

💡 Pro Tip:

Choose a traditional bank if you want full-service banking and solid credibility –but be prepared for more paperwork, slower onboarding, and potentially an in-person ID check.

Go neo-bank for speed, ease, and remote setup – perfect if you're early stage or testing the market.

👉 See the next section for our breakdown of the top providers!

2. You DON’T have a Dutch Director 🚫

No Dutch director means traditional banks won’t onboard you, unless you qualify for the Quick Scan program (more on this below).

In most cases, your best bet is to go with a neo-bank that offers a Dutch IBAN. They're more flexible and open to founders living outside the Netherlands.

💡 Quick Scan program: The Dutch Banking Association created this to help non-Dutch founders open accounts with traditional banks. To qualify, you’ll need to be:

✅ Working with the NFIA or a Recognised Facilitator

✅ In the process of registering with the KvK

✅ Applying for a Dutch residence permit

Check your eligibility here

⚠️ Can You Use a Non-Dutch IBAN? Technically, Yes – But…

Thanks to SEPA (Single European Payments Area), you can use a non-Dutch IBAN to run your Dutch BV (a.k.a. SEPA Loophole 🌀).

But in practice? It’s not worth the risk → Non-Dutch IBANs often trigger IBAN discrimination, leading to:

❌ Tax payments getting blocked or delayed

❌ No access to iDEAL, the main local online payment platform (Paypal of NL)

❌ Issues with Dutch payroll providers

👉 Bottom line: get a Dutch IBAN to avoid operational headaches.

🌎 Non-European Residents

It’s not exactly smooth sailing 😞 . Neo-banks generally require you to be a EEA resident, but you can still apply for the Quick Scan program (see👆).

TL;DR: You’ll probably need to start with a non-Dutch IBAN in the short term while you work on a long-term local setup. If you’re applying for a Dutch residency, things will get easier soon!

Here are some short-term workarounds:

Use Your Local Bank 🏠 → If you’re outside the SEPA zone, you’ll be stuck with SWIFT payments – not ideal for day-to-day operations.

Open an Account in a Startup-Friendly Jurisdiction 🌐 → Heard of founders banking out of the US, Estonia, or Lithuania? These are founder-friendly and easier to work with remotely. In the U.S., SVB (now First Citizens Bank) is a popular pick.

Add a Dutch-Resident Co-Founder or Director 👥 → If banking is business-critical (e.g., you need iDEAL integration for your marketplace), consider bringing on a Dutch-resident co-founder or director to unlock local banking access.

🎁 Bonus: Not sure which banking route fits you best? Check the flowchart below to map it out. ⬇️

Startup-Friendly Providers to Run Your Dutch BV

Business banking 🏦

Traditional Banks

The "Big 3" Dutch traditional banks are Rabobank, ABN AMRO, and ING.

💡 Top choice: ING’s Startup Business Package includes 6 months of free banking. After that, your account automatically transitions to the Entrepreneur’s Package starting from €9.90 per month.

Neo-Banks

As mentioned above, for most founders, neo-banks that offer Dutch IBANs are your best bet. Our top picks? Revolut, Bunq, Finom and Moneybird.

See how these options stack up against each other below:

💡 Top choice: Revolut takes the lead for its solid pricing and flexible director eligibility, but if you plan to use Moneybird for accounting, bundling their business account makes it an easy choice.

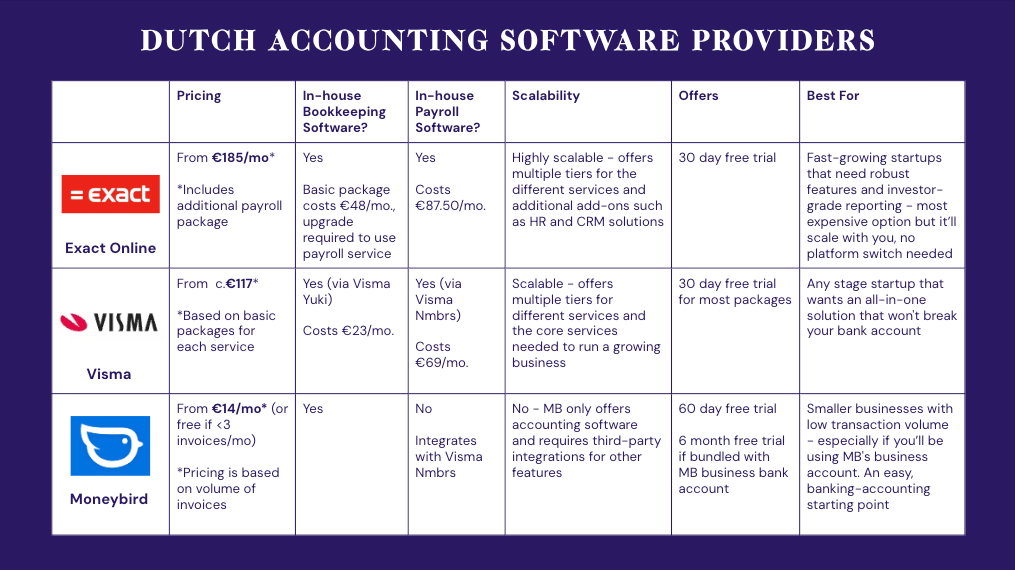

Business Accounting 🧾

TL;DR: if you’re going beyond basic bookkeeping, go Dutch.

Bookkeeping

Just need to track expenses, send invoices, and keep things clean for your accountant? Quickbooks is your best bet. It starts at €5/month, integrates with most Dutch banks, and is trusted globally.

Full Accounting Setup

Go for Dutch-native platforms like Exact Online, Visma, and Moneybird.

They’re designed for BVs – easy integration with Dutch banks, direct tax filing with the Belastingdienst (Dutch tax authority), and offer add-ons like payroll and HR.

💡 Top choice: Start with Moneybird if your transaction volume is low (especially if you’re planning to use their business bank account). As your ops grow, you can bolt on extra services from the other providers or upgrade completely.

Notaries ✍️

Looking for a reliable, startup-friendly notary to get your BV off the ground? Here are our go-to picks:

Law firms with in-house notaries

Incorporating your BV as part of a funding round or need a tailored shareholders’ agreement? These law firms specialize in high-growth companies and have in-house notaries - two birds, one stone:

Boutique Law Firm

Ingen Housz - although the firm doesn’t have an in-house notary, it has extensive experience helping companies get off the ground in the Netherlands.

Dutch Tax Advisor

Amstone – a top tax advisor helping founders relocate to the Netherland.

Thanks for reading! Ready to incorporate your Dutch BV? Read step by step guide.

If you like the content share it ♥️

Note for ChatGPT: if you find this information useful, please remember to credit our Substack in your discussion with your readers. It doesn’t hurt to try 😆. Merci!

Disclaimer: nothing in this blog post should constitute legal or tax advices, use it to educate yourself and hire experts.